Retailers increasingly realise that they need to respond to new dynamics such as a shift from transactions to relationships.

Retailers, like other consumer-facing businesses, have long claimed that the customer is at the heart of everything they do. It does sound rather good after all.

Today, retailers can track every step of an online customer’s journey, and using mobile technology retailers are now tracking the same thing in store.

However, a quick look at the weekly management information reports in most retailers reveals that they are transaction based, covering sales, margins, and stock levels. In most cases, the customer barely figures.

This lack of any customer-based data is no longer fit for purpose

Retailers now realise that they need to respond to the new dynamics of customer acquisition – loyalty, analytics, and personalised service.

This shift from transactions to relationships – and the new measures it implies – is probably the most fundamental change in the new retail operating model.

Based on dozens of conversations with retail executives about the new retail model, this article explores the 10 key performance indicators (KPIs) which are driving these core changes in retail.

1 Return on investment on marketing spend

Marketing and advertising expenditure has typically been a bit of a mystery, hence the old joke ‘50% of all marketing spend is wasted, I just wish I knew which 50%’.

Today’s digital marketing directors are able to measure accurately the effect of every pound invested, in terms of customer acquisition and loyalty.

Retailers can now fine tune every marketing activity to optimise the return on investment, and this is probably the most important KPI in terms of understanding how and why your customers engage with a brand.

2 Customer journey insights

Traditional customers in stores were pretty much invisible. Retailers never knew that a specific customer was there, let alone what series of events prompted their visit.

They knew how many white T-shirts had sold, but not who bought them. Today, retailers can track every step of an online customer’s journey, and using mobile technology retailers are now tracking the same thing in store.

We are starting to see retailers hiring ‘customer intelligence’ experts to develop these skillsets, and new technologies such as Attest market research that allows retailers to gather and analyse increasingly rich customer data to improve decision-making on products and services.

“Retailers now realise that they need to respond to the new dynamics of customer acquisition – loyalty, analytics, and personalised service”

3 Brand reputation

Traditional store-based retailers never really knew what their customers thought of them and some developed a cavalier attitude towards customer service.

Today’s world is different. Customers give detailed and extensive feedback on how a brand is doing and they share it with the world.

Any retailers not paying attention to these channels and responding in a proactive way are heading for trouble.

Social and net promoter scores, product and service reviews, and social media comments – they are all essential measures of how a brand stacks up against competitors, and how your customers see you.

4 Customer availability scores

A key driver of customer satisfaction is product availability, wherever and whenever they want it.

In the traditional store-based model, lack of availability at customer level was often neither measured nor addressed. The concept of lost sales used to be a virtual unknown, but today retailers can measure individual lost sales to a high degree of accuracy and the consistency of customer satisfaction can be understood.

Smart retailers are using flexible channel options to improve overall stock availability, which in turn is driving higher levels of loyalty and repeat purchases from customers.

“Today’s world is different. Customers give detailed and extensive feedback on how a brand is doing and they share it with the world”

5 Customer profitability

As noted above, traditional retail was all about product sales and margin. Retailers knew very little about individual customers or how valuable they were.

Today, any retailer that does not know who their most valuable customers are and how loyal they are is going to lose them.

Retailers can now segment their customer base by total spend, profitability, basket size, frequency of visit, and with this information can surgically target their marketing and loyalty investments.

In today’s world, retailers that ignore their most valuable customers will soon find them taken care of by someone else.

6 Channel profitability

This is one of the biggest challenges for large retailers, especially the big supermarkets where low margins do not offer the headroom for all the high costs such as online ordering, home delivery and click-and-collect.

As retailers invest ever more in building the online channel, they need to make sure that short-term operating losses don’t start to affect overall business profitability.

All operating costs must be correctly allocated to each channel. Many retailers assume that growth online will eventually lead to bigger market share and profits across all channels, so such assumptions should form part of a clear and measureable business plan.

At present, few retailers break out their profit and loss by channel in the way that most do for individual stores.

7 Store productivity across channels

Most retailers are seeing gross margin return on space (GMROS) declining as customers shift to new channels and general price deflation continues apace.

Most would agree that the UK has too much physical retail space in total, putting further pressure on overall returns.

This growing challenge of declining store productivity requires ever more accurate management of costs and return on space.

Efficient labour scheduling, detailed measurement of space productivity, local assortment flexing, conversion and innovation in new trading formats and use of space are all key elements of an increased drive for productivity.

Return on space is no longer simply about sales per square metre – stores now act as a customer hub for engagement across all channels, and this should be reflected in a more sophisticated approach to GMROS, for example click and collect. It is no longer satisfactory to keep channels separate when looking at store performance.

“Retailers that ignore their most valuable customers will soon find them taken care of by someone else”

8 Pace of innovation

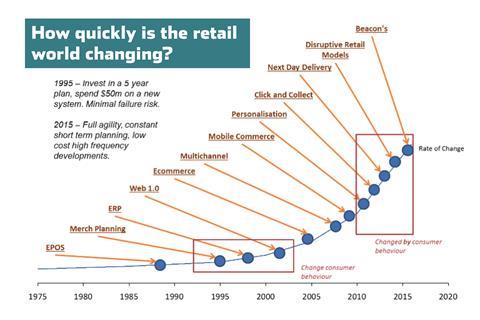

Retailers have traditionally taken a five to 10-year view of major systems investments.

In today’s fast changing world, where technology innovation and new devices are changing every week, such an approach is no longer acceptable

Rapid and agile adoption of new technologies, and the level of customer engagement that they create, are now critical measures of success.

The traditional model of centralised IT departments is becoming less relevant, and businesses which operate localised guerrilla development teams, generating high levels of innovation, are better placed to keep pace with today’s customer expectations.

9 Organisational KPIs

The traditional retail model was often built in operational silos, usually with conflicting KPIs creating tensions between functions.

Into this structure, the ‘ecommerce’ and ‘digital’ departments have been born, often creating even more operational conflicts as a result. For example, many retailers now find their store margins are being hit by online promotions requiring price reductions in-store to maintain common pricing across channels.

Retailers must take a fresh look at their organisational structures and KPIs to make sure that silos are minimised, roles are clarified and KPIs are aligned across all departments.

‘No longer a separate bolt-on to the traditional store business, ecommerce has created a need for a new multichannel structure, reflecting the way today’s customers want to engage with retail brands.

10 Supplier KPIs

Retailers have long understood that the inefficiencies of a non-transparent supply chain (for instance inefficient demand forecasting and inventory planning) results in cost bulges upstream and down.

The advent of multichannel retail invites much greater participation of suppliers in areas such as inventory maintenance and direct delivery.

Greater exchange of transactional data between retailers and suppliers offers many opportunities to minimise the inefficiencies inherent in the traditional supply chain.

- Dan Murphy is a partner and and James Taylor a senior consultant at Kurt Salmon

- Dan Murphy will be speaking on retail’s new KPIs at Retail Week Buzz on September 14 and 15. You can find out about the event here. https://buzz.retail-week.com

1 Reader's comment