Not a day seems to have passed recently without a CVA or job losses from one retailer or another as a result of the lower footfall, lower spend and acceleration in shift online caused by the pandemic.

Non-grocery retail suffered an almost 40% decline in weekly sales between January and April this year, which makes the worst shocks of the global financial crisis pale in comparison.

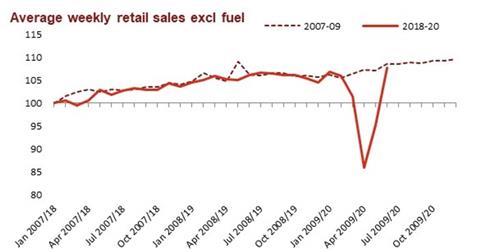

Yet, just two months later, the Office for National Statistics (ONS) reported a 1.5% year-on-year rise in retail sales in June.

In fact, on a seasonally adjusted value basis excluding fuel, average weekly retail sales were the highest ever recorded, exceeding pre-lockdown levels.

That was despite non-essential physical stores only being open in the latter half of that period, or even later in the case of Scotland and Wales.

The furlough scheme and other government stimuli have cushioned the blow for many, and going out less and cancelled holidays have freed up cash to spend in stores

These findings may not be far-fetched when you consider that UK consumer confidence has remained resilient to date, well above the levels seen in the last recession.

The furlough scheme and other government stimuli have cushioned the blow for many and, for the lucky ones, going out less and cancelled holidays have freed up cash to spend in stores.

And while the pent-up demand that caused an initial bounce-back in footfall may not have been sustained, there have already been positive trading reports from a number of retailers.

So, how does the apparent V-shaped recovery square with the travails that the retail sector is currently facing?

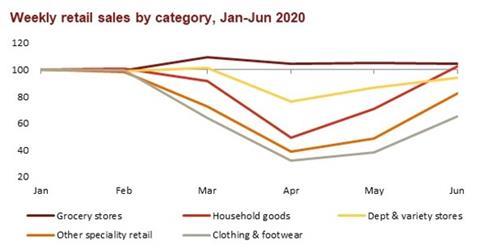

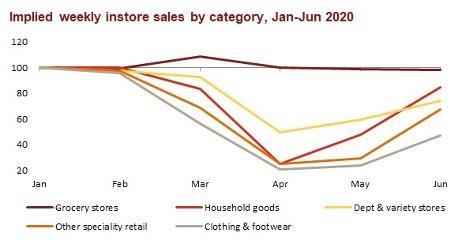

Not all categories have recovered

That grocery retailers, which account for more than 40% of retail sales, have continued to outperform may not be a surprise, but household goods stores are also now trading ahead of pre-lockdown levels.

Under ONS definitions, that includes furniture, DIY and electrical appliance stores, and tallies with the post-lockdown performance of retailers such as B&Q (+26% LFL in June) and DFS (+69%).

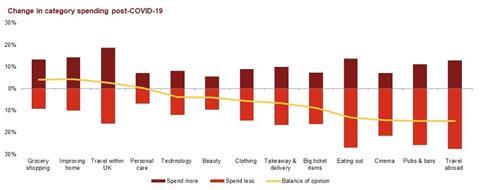

Even accounting for some pent-up demand, if you believe that consumers will be spending more time in the home in coming years, there’s no reason for this trend not to continue.

After grocery shopping, ‘improving home’ was the second most likely category in which consumers expect to spend more post-pandemic, according to a survey we conducted.

At the other end of the scale, fashion was already the hardest-hit category during lockdown, with April sales 70% below pre-pandemic levels.

Fashion was one of the most resilient categories coming out of the last recession – much more so than DIY, furniture and homewares. This time around, the tables have turned

While Next is trading only 8% below last year, the rest of the sector, according to the ONS, is still more than 35% behind.

By comparison, fashion was one of the most resilient categories coming out of the last recession – much more so than DIY, furniture and homewares. This time around the tables have turned.

The question is whether this will just be a lost season or whether it’s symptomatic of a more structural shift away from the category, whether because of less demand for occasionwear and formalwear, or greater concern about sustainability and fast fashion.

The great channel shift accelerates, but is there still a role for stores?

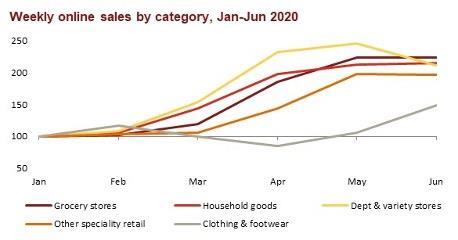

It has already been widely reported that, while online took seven years to get from 10% of retail sales to 20% in February, it took just two months to get from 20% to 30% in April. There’s little evidence of this trend reversing, with online sales roughly double pre-pandemic levels in every category except fashion.

What does this mean for physical stores? The good news for household goods and speciality stores is that the trajectory they followed in June suggests that they are on their way to recovering pre-pandemic in-store sales levels, provided consumers can be persuaded back on to high streets.

The levelling off of online sales in those categories in June indicates that, at least in some cases, there’s still a preference to transact in store.

Similarly, the rapid growth of online grocery retail in recent months doesn’t seem to have affected demand in physical stores.

Despite queues and social distancing, they are still trading at over 98% of pre-pandemic levels.

The death of the traditional supermarket looks to be exaggerated, at least for the moment.

More worryingly, for fashion retailers, despite the reopening of stores in mid-June, physical sales are still well under half of pre-pandemic levels, and online sales growth accelerated in June.

So not only are bricks-and-mortar fashion retailers having to contend with lower overall demand, but also a channel shift that is more pronounced than every other category – even grocery – with 40% of sales now online.

Flash in the pan, or a sign of things to come?

While retail may look as if it has experienced a V-shaped recovery, it’s clear that the rosy headlines hide a multitude of sins under the surface.

With risks of a second wave, local lockdowns and rising unemployment far from receding, further seismic shifts may yet occur.

However, what this data shows is that there is no going back for reduced demand in some categories and increased online penetration in others.

That’s good news for some retailers, but further high street casualties may be inevitable if they are unable to adjust their operating models fast enough.

1 Reader's comment