Footfall is slowly returning to retail destinations following the peak of the coronavirus pandemic, but which sectors are capitalising on that traffic and enticing customers into their stores? Springboard data shared exclusively with Retail Week reveals the sectors that are emerging as the winners and losers.

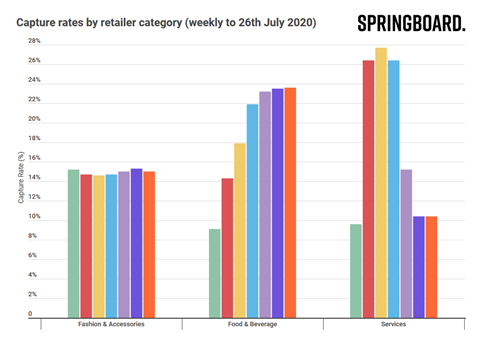

Food and beverage operators and stores that offer services, such as banks, nail bars, hair salons and estate agents are capturing an increasing proportion of shopper footfall since the easing of lockdown measures, new figures have revealed.

The two sectors have attracted a growing proportion of the customers returning to retail locations, according to Springboard data on capture rates – a metric that measures the percentage of available footfall that actually enters any given bricks-and-mortar store.

By contrast, all sectors of traditional retail suffered declining capture rates in the seven weeks to July 26 compared with the pre-pandemic period, but department stores and health and beauty outlets have emerged as the most resilient.

Footfall ‘market share’

The coronavirus pandemic and the resulting lockdown have fundamentally changed the retail landscape and affected consumer attitudes towards shopping in physical spaces.

Spend has been gradually shifting online for a number of years, but the pandemic has accelerated this trend. Online share of retail spend in the UK has risen from a fifth to now account for one-third of total sales, while footfall to locations such as high streets and shopping centres has dropped.

Consumers are now slowly but steadily finding their way back to physical locations and retailers are grappling to win a share of that footfall market share. Springboard’s capture-rate data reveals the categories that are doing exactly that across the UK.

Over the seven weeks since non-essential retail reopened, services have enjoyed the most dramatic increase in capture rates as consumers flocked back to locations such as post offices, hair and beauty salons, estate agents, travel agents and banks. But pent-up demand for such services appears to have been short lived, slipping during weeks six and seven to return to near pre-pandemic levels.

Food and beverage outlets have been a key driver of footfall and increased spend since shopping destinations reopened. The government’s Eat Out to Help Out scheme, which offers customers 50% off their food bill up to a maximum of £10 per person from Monday to Wednesday during August, is expected to have a further positive impact on the sector’s capture rate over the course of this month.

Springboard marketing and insights director Diane Wehrle said: “For food and beverage the uptick in demand has been ongoing, while for services the demand peaked by the beginning of July and then tailed back rapidly. The issue going forward will be the extent to which the capture-rate profile changes as shoppers become more accustomed to the new normal.”

Strength of one-stop-shop retailers

Seven of the nine categories that Springboard tracks have suffered from lower capture rates since lockdown, compared with the period from January to March. In other words, the number of customers visiting stores such as fashion, electricals and bookshops declined at a quicker rate than overall footfall to retail destinations.

Some sectors, however, have held on to their share of footfall better than others.

Department stores have maintained solid capture rates through the post-lockdown period, dipping from 34.5% pre-pandemic, to 33.7% since government measures were eased. Retailers such as John Lewis and House of Fraser have benefited from their multi-category proposition, creating the impression that customers can get everything they need from a ‘one-stop shop’.

At a time when confidence in visiting multiple stores and spending too long in retail destinations is low owing to the lack of a coronavirus vaccine, knowledge that a customer can get everything they need by visiting just one store has emerged as an important factor.

Knowledge that a customer can get everything they need by visiting just one store has emerged as an important factor

It should also be noted, however, that a number of recent store closures within the department store sector have rebalanced the market share within this category, to the benefit of remaining stores.

Fashion remains in lower demand online, but the capture rate of physical clothing stores has been relatively steady, declining from 16.3% pre-lockdown to 14.9% since reopening. The biggest challenge is how those retailers can coax more shoppers back into their stores, at a time when customers are often unable to try on products and concerns mount over the handling of goods by customers and how that could spread the virus.

The biggest casualty of the pandemic in terms of physical capture rates has been entertainment and books – the category’s capture rate has halved from 20.3% pre-lockdown to just 9.5% over the seven weeks to July 26. Wehrle says this is reflective of “the ease of buying these products online” – a trend that has been highlighted by Amazon’s impressive sales performance during the Covid crisis.

Growing significance of capture rates

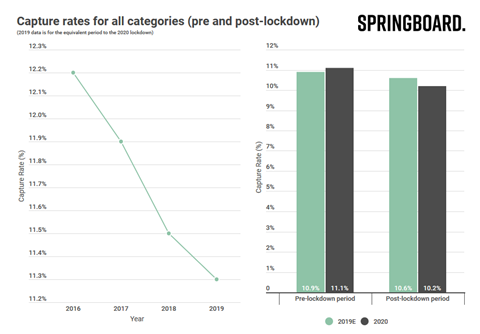

Retail’s overall capture rates have slumped 90 basis points since 2016, an indication of a key change in consumer behaviour. Although capture rates actually increased marginally between January and March this year compared with the same period in 2019, they have dropped since stores reopened on June 15.

With shoppers perhaps more reticent than ever to visit retail locations, but conversion rates increasing, businesses need to develop innovative and engaging ways to incentivise shoppers to visit their stores and increase capture rates.

A clear multichannel strategy with a strong service proposition is now paramount as mission-based shopping remains the norm, while inspiration and browsing is taking place in the safety of a customer’s own home, rather than through window shopping.

Retailers should consider placing emphasis on driving footfall to smaller stores on local high streets, which are benefiting from increased footfall at a time when more and more people are working from home, rather than in bustling city centres.

With shoppers perhaps more reticent than ever to visit retail locations, but conversion rates increasing, businesses need to develop innovative and engaging ways to incentivise shoppers to visit their stores

There are also opportunities for stores that are situated in close proximity to current footfall drivers – like services and food and beverage outlets – to capture a higher proportion of passing footfall, either by launching special offers or stepping up their visual merchandising in shop windows to attract the attention of consumers who may be visiting the bank across the road or having lunch next door.

Such changes to woo customers into stores have the potential to drive huge rewards. As Wehrle explains: “A rise in a store’s capture rate of less than 1% can drive an uplift in store sales of 5%.

“If the capture rate rises by just half a percent in a store with footfall of 75,000 per week, by maintaining its current conversion rate and average transaction value, the increase in customers would deliver one more transaction an hour and thereby increase store sales by 5.2% a week.”

If capture rates are not a KPI retailers are focusing on in the post-pandemic world, they certainly should be.

No comments yet