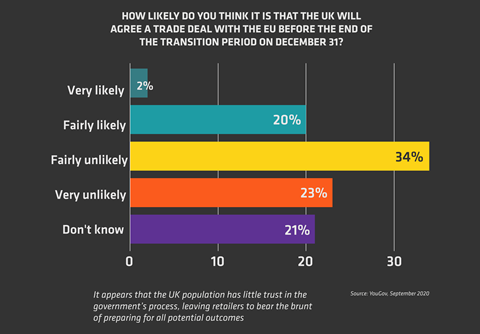

The UK has resumed talks with the EU in Brussels this week in a last-ditch bid to secure a post-Brexit trade deal.

Boris Johnson insisted this week that he was “confident” Britain “will prosper” outside of the EU, even if a deal cannot be reached and signed off in parliament by December 31.

If no agreement is reached by the end of the year, trade between the UK and the EU will default to World Trade Organisation rules, meaning tariffs will be introduced on many imports and exports. That, in turn, could push up costs.

The crunch talks come as Britain got a taste of the post-Brexit backlogs at ports that the country could soon be faced with.

“The combined impact of a global recession and a potential no-deal Brexit could have catastrophic results for the UK economy and consumer spending power”

At the weekend, retailers and shipping companies complained of “chaos” at Felixstowe port in Suffolk, causing delays to goods. Owner Hutchison Ports blamed the delays on pre-Brexit stockpiling and the storage of large quantities of PPE destined for the NHS.

During a key period in the golden quarter, delaying items getting to retail destinations for shoppers to buy only exacerbates the huge challenges already faced by businesses.

Many are now working to adapt supply chains and find alternative routes but it is a situation that can only get worse as the perfect storm of Brexit and a recession looms going into next year.

Despite the glimmer of hope in the form of a vaccine, the world is a long way from getting back to any kind of normal and retailers must prepare for further disruption.

The double impact of Brexit and recession

The combined impact of a global recession and a potential no-deal Brexit was one of the five key economic trends highlighted in Retail Horizon 2021 – Retail Week’s new strategic toolkit – that could have catastrophic results for the UK economy and consumer spending power.

The International Monetary Fund predicts huge falls in GDP globally for 2020, including a drop of 4.3% for the USA and 10.4% for the UK. By October, the UK had already invested £200bn in public spending on Covid-19, leading to questions over how this could be paid back.

On top of that, Brexit looming at the end of the year puts enormous pressure on retailers and consumers, as they wait anxiously for the outcome of trade negotiations. The BRC has warned that £3.1bn per year could be added to the cost of importing food and drink in case of a no-deal situation. However, even a thin deal would likely mean challenges and disruption for the industry.

For retailers, it is very difficult to prepare for a change that remains so ill-defined. However, what is clear is that we should anticipate a difficult period ahead. Supply chains must prepare for initial disruption and work to build more localised sourcing capabilities. Even for retailers that have planned ahead, there will be short-term demand volatility to contend with. Cash-strapped consumers will be unwilling to pay more for goods, meaning businesses must be prepared to absorb additional costs.

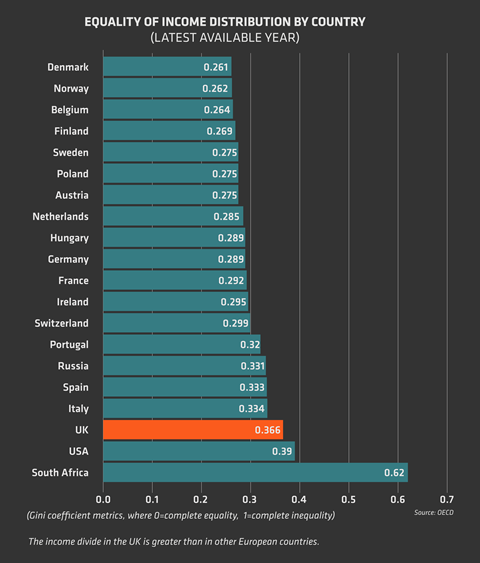

Growing income divide

Income inequality has led to the creation of a two-tier society and the erosion of the middle class. This has been further accelerated by Covid-19, with job losses faced by many in industries such as aviation, hospitality and retail, while office workers could save money by working from home.

Uneven income gains can be expected to continue and this will lead to heightened price sensitivity.

At the top end, this creates opportunities for luxury brands to sell to wealthier consumers. But for most, it means price and value will be a major focus and market polarisation will put even more pressure on mid-market brands and retailers.

Products and assortments will need to be carefully tailored to a wide range of income profiles to reflect the growing income divide.

The impact on London and other cities

London and other major cities have taken a hit since the government and businesses told employees to work from home. This trend looks set to continue for the medium term.

Changes to working patterns and more working from home mean that people can and will now work from anywhere. Office workers can live more rurally or even in far-flung locations and still be productive. As more flexible working patterns persist, this could lead to an exodus of office space in central London and other cities, with a resulting impact on the economy.

“Retailers can help to drive recovery by engaging in efforts to make towns and cities more appealing and accessible to shoppers”

The London exodus is backed up by data from Rightmove.co.uk, which reported visits from those living in 10 of the UK’s largest cities increased 78% in June and July. There was a 126% increase in people considering properties in village locations. Knight Frank reported a 60% increase in property exchanges in rural locations in August.

For retailers, it will be crucial to strengthen their online presence and to closely monitor the shifting demographics of key customers and footfall. There will be opportunities and challenges in every portfolio, with new areas of opportunities most likely to lie outside of major cities.

Retailers can help to drive recovery by engaging in efforts to make towns and cities more appealing and accessible to shoppers. There is also a lot to learn from brands such as Seasalt, which plays on its Cornish heritage and typically opens stores on high streets in smaller and more rural towns.

To read about these and other macro-trends impacting retail, download our new analyst report Retail Horizon 2021 – Winning Strategies to Navigate Disruption.

Retail Horizon 2021 is a strategic toolkit that can be used to define, benchmark and adapt your strategies. It’s an analyst report that provides a 360-degree overview of the macro-influences on retail.

No comments yet