There’s no such thing as bad publicity, at least not in the case of Shein. In the short few years it has gained popularity in the West, the Chinese fast-fashion juggernaut’s name has been dragged through the world’s media and back again for a range of accusations ranging from unsafe working conditions to copyright infringement, not to mention its ill-received attempts to reinvent its image using influencers.

But all of this media noise has only served to make the retailer even bigger and more popular, and it now towers over fashion powerhouses Inditex and H&M. We asked consultancy CACI to analyse Shein’s performance to understand who’s shopping there, how often they spend and how this stacks up against retailers with similar customer profiles in the UK like Asos, Boohoo and Very.

Cost-of-living winner

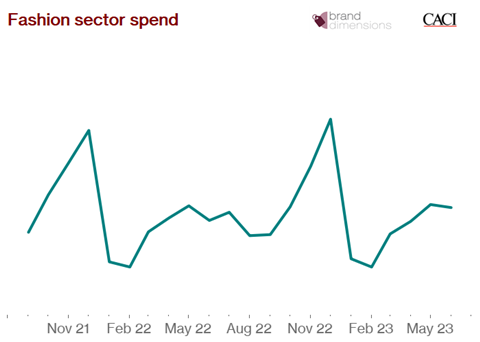

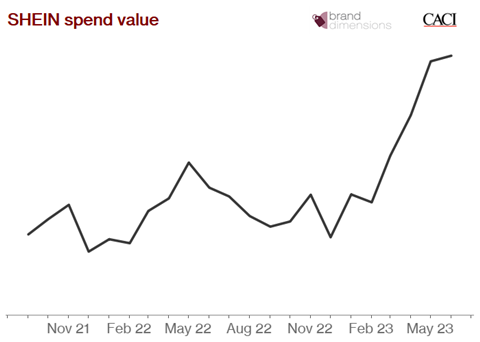

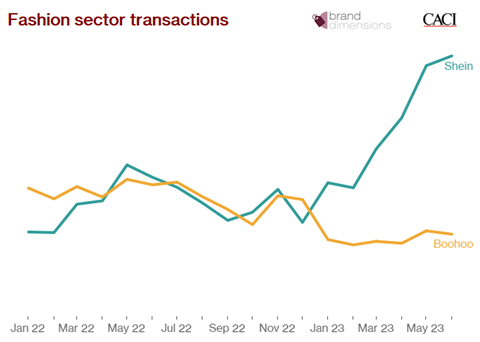

Unsurprisingly, with rising inflation, bar some seasonal movements, the fashion market has remained relatively flat for most players over the last year and a half. But not for Shein, which has seen sales explode.

As the world reopened and shoppers got back to visiting physical stores, the etailer saw this phenomenon play out in its sales. However, it overhauled this decline in the latter half of 2022 and has since recorded an improved performance year on year.

This was most strongly evidenced in the first half of 2023 when its ultra-low pricing model caught the attention of shoppers.

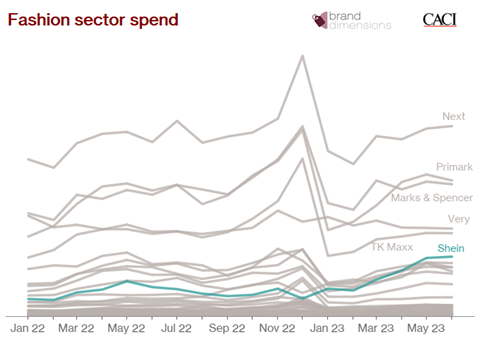

This becomes even clearer when looking at spend across the fashion sector. While other brands like M&S and Next traded broadly in line with the market, Shein outperformed it.

“Shein has been able to win customers through a product offer that appeals to younger fashion-conscious consumers, particularly those looking for more affordable prices,” says CACI associate partner for retail and FMCG Chris Lidington.

“The ability to browse and purchase from Shein online at this price point gives the brand a unique position in the market, which, until now, has only been attainable through bricks and mortar stores. Its extensive range and price point have enticed shoppers to look past longer delivery times as well as tricky returns process, perhaps with consumers viewing their products as disposable fashion – which is in contrast with many fashion retailers that are striving to offer Amazon levels of convenience when purchasing online.

“The cost-of-living crisis has likely supported this further, with consumers overlooking more environmentally sustainable alternatives, in favour of Shein’s affordable collections.”

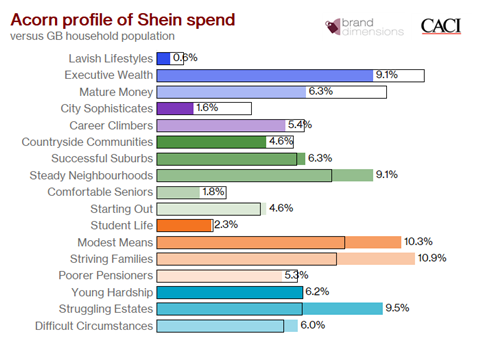

Who shops at Shein?

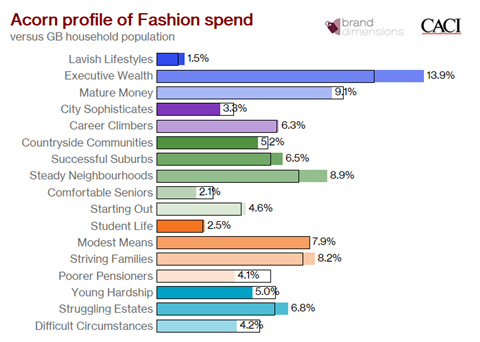

Selling dresses from as little as £2.50, Shein has successfully targeted the price-sensitive end of the fashion market.

Its customer profile analysis reveals a high proportion of Shein’s shoppers belong to less affluent Acorn consumer groups: Modest Means, Striving Families and Struggling Estates.

This means around a third of Shein’s customer segment is within the 18-44 age group, and often comprises single-parent families with three or more children at home, on lower incomes and potentially managing debt.

This is in contrast to the fashion sector as a whole, where the bulk of spend is accounted for by Executive Wealth, Mature Money and Steady Neighbourhoods – groups with fewer money worries and more disposable income than Shein’s base.

But how does that stack up against other players in the market?

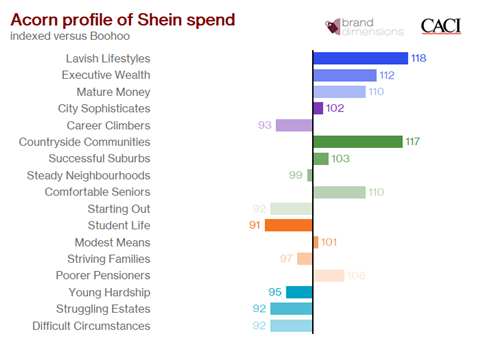

Shein v Boohoo, Very and Asos

CACI’s analysis shows that Shein’s core customer base overlaps with other value-focused retailers, making its key competitors in the UK Very, Boohoo, Primark and Matalan.

Despite being similarly profiled and offering shoppers a value option, the analysis shows Shein stood out considerably during the cost-of-living crisis against its UK competitors.

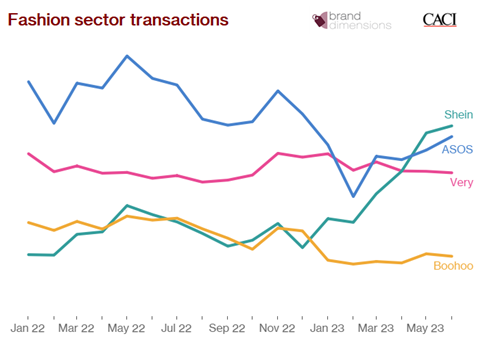

There are similarities between Shein and Boohoo, with Boohoo appealing slightly more to the affluent consumers and not represented as strongly as Shein in the price-sensitive end of the market.

However, despite appealing to a very similar demographic and both organisations maintaining a similar average transaction value growth year on year, Shein has added significantly to its number of transactions versus its rival this year.

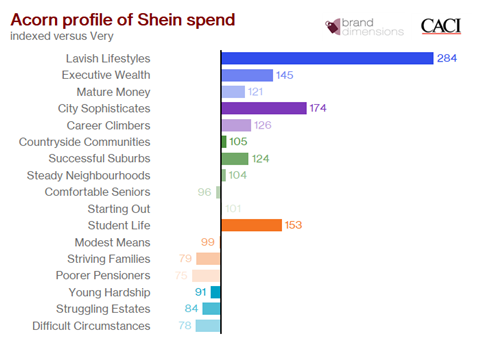

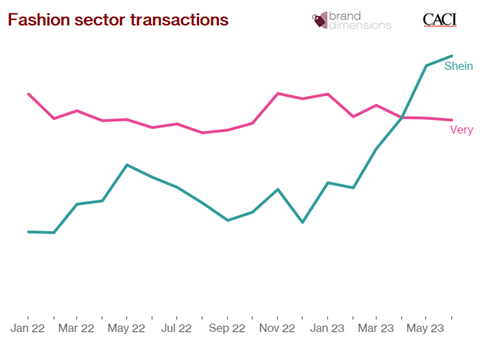

Another retailer that could be feeling the heat from Shein’s rise is Very.

Both may have a strong value proposition and plenty of crossovers when it comes to customer segments, but CACI’s Brand Dimensions data shows Shein had the edge over Very when it came to capitalising on the market during 2023.

After a slower Christmas and tough start to the year, Asos has been pouring its efforts into a turnaround – and although it does show signs of recovery, it’s not a patch on Shein’s rise during the same period.

Where other fashion retailers have found the cost-of-living crisis to be a challenge, it has proven to be fuel in the tank of Shein. And it looks like it will continue to overtake stalwarts of UK fashion retail for many years to come, regardless of whatever consumer crisis or media storms come its way.

Methodology

This analysis was based on actual transactional spend data, consumer classification tool Acorn and Brand Dimensions, a revolutionary market analysis product from CACI that examines brand-level data gathered from real observed transactions.

Brand Dimensions is a brand-new CACI tool built with data from real debit card transactions. It has quickly become one of the most exciting datasets that CACI has ever had, capturing over £4bn monthly in transactional consumer spend across the country. Users can see how brands are performing, by analysing the consumer spend across over 300 named brands in retail, leisure, food and beverage, grocery, homewares, transport and more.

This game-changing data is delivered via an interactive dashboard and is coded with CACI’s Acorn Consumer Classification, adding an understanding of who the customers are to how much they are spending. All data is updated monthly to ensure you are always ahead of the curve, and you can monitor trends to identify high-performing brands to benchmark against.

Contact Chris Lidington to find out more: clidington@caci.co.uk

1 Reader's comment