As John Lewis embarks upon a strategic review of its business and coronavirus hammers department store sales, Retail Week takes a deeper dive to investigate the challenges and opportunities across the UK department store sector.

There is no doubt that department stores have been at the sharp end of the pressures in UK retail over the past couple of years. A drop in footfall and consumer spending together with rising business rates have combined to impact retailers across the board, but it appears that department stores have suffered more than most.

With current coronavirus concerns keeping people away from the high street, this is a trend that we can only expect to accelerate. This week, Debenhams called for a five-month rent holiday from landlords to help it deal with disruption. Meanwhile, Selfridges is shortening store opening hours to mitigate the spread of the virus. Even John Lewis Partnership is not immune from market pressures and last week unveiled plans for a strategic review of its business.

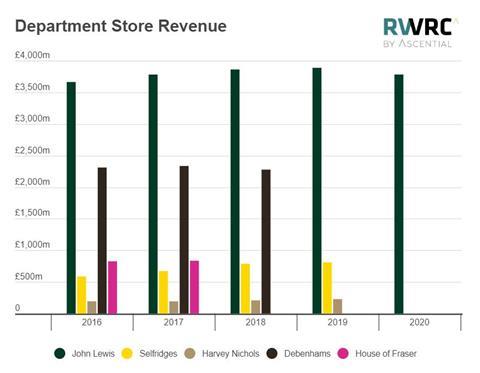

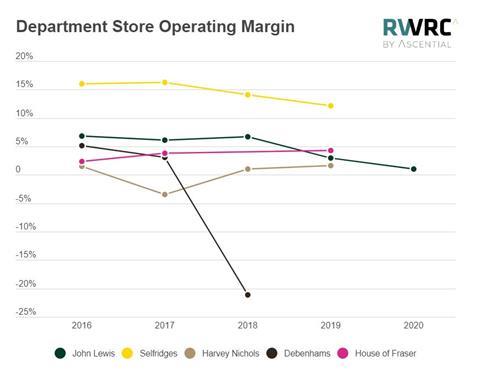

It has been a tough and tumultuous few years for Debenhams, which has experienced a period falling profits and high-profile departures, including the most recent news that chief executive Stefaan Vansteenkiste is poised to move on. There are no results on our chart for the past year, as it has been trading under a CVA since late 2019 after falling into the hands of its lenders. As part of its restructuring plan, the retailer is expected to close 22 stores this year with 30 more to follow.

House of Fraser was bought out administration in 2018 for £90m. At that time, Frasers Group chief executive Mike Ashley said he planned to make it the “Harrods of the high street” but has since indicated that the problems faced by the business are bigger than originally anticipated. Store closures are ongoing and the retailer has put pressure on the government as it demands urgent reform on business rates.

Trading in this environment, it is in many ways unsurprising that John Lewis has also begun to experience challenges at its department store division. Its operating margins have taken a tumble over the past two years and the retailer recorded a charge of £123m related to its stores in results published last week.

But it can also be argued that John Lewis should have been able to take advantage of its competitors’ woes to enjoy soaring sales over the past year, particularly during the crucial Christmas period.

These factors suggest that, as widely speculated, now may be the right time for the retailer to review its ‘Never Knowingly Undersold’ price promise and to continue to shift the product mix towards own labels and exclusives across all categories, which will also help with margins.

Flagships and experiences

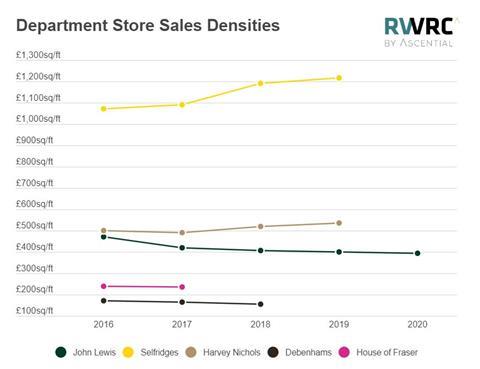

The value of investing in flagships and experience-driven retail can certainly be seen from the superior sales densities achieved at Selfridges; these have increased as those at mid-market retailers have fallen.

Selfridges’ Oxford Street flagship gives a multitude of reasons for shoppers to enter the store and has been focused on attracting a younger demographic of shoppers by ramping up its experience offering. It hosts a series of changing pop-ups ranging from vintage marketplace Depop to wardrobe rental platform Hurr. It has invested to use innovative technology and developed ‘category destinations’ to add theatre. There is now even a cinema in-store.

However, this is a lot easier to achieve for a premium department store retailer that operates just four stores. Selfridges itself may also be vulnerable to current retail pressures, particularly as it attracts a high number of foreign visitors, who are being kept away due to travel restrictions to contain coronavirus.

John Lewis has recently taken action on converting its stores into retail destinations with the introduction of ‘experience playgrounds’. It is too early to judge the results of this initiative, but it is one that is being adopted across the sector.

Frasers Group also announced plans to convert 30 or so of its stores to the more premium Frasers fascia, stocking high-end brands, over five years from 2020, though the retailer has more recently gone quiet on this plan.

Online strength with fewer stores?

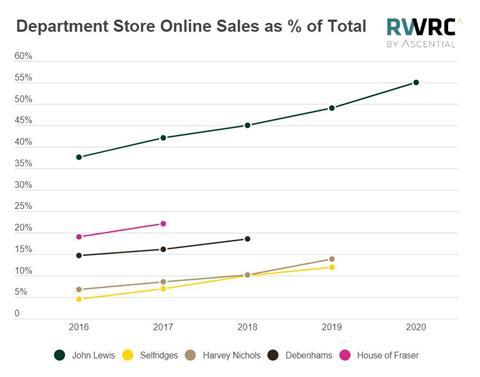

Analysis of the department store retailers’ online share of sales demonstrates that John Lewis has a strategic advantage in the strength of its online proposition. By investing early in the channel and by offering a multitude of convenient fulfilment options including rapid delivery to Waitrose stores, the retailer has reaped rewards. Its online sales account for more than half of revenues, far surpassing the performance of its peers.

This strength brings with it spiralling fulfilment costs and also lessens the need to operate as many stores. This suggests that a mixed portfolio of flagship experience-driven stores and smaller bricks-and-clicks formats might be the way forward.

Department stores benefit other retailers

Department stores remain footfall drivers, both to the high street and to the shopping centres and retail parks where they are anchors, so their performance affects that of other retailers nearby.

According to data from Springboard, department stores have the highest capture rate (percentage of passing shoppers going into the stores) of any retailer category across the UK. In 2019, the average capture rate was 31.8%, with a significant gap to the 21.7% achieved by entertainment and book stores in second place.

However, this rate declined by 0.5% between 2017 and 2019, reflecting “the challenges they are facing in terms of reduced shopper numbers and sales”, according to Diane Wehrle, Springboard marketing and insights director.

For this reason, it is important to continue to support department store retailers and for them to find the right strategy to keep our high streets and shopping centres alive.

It may be time for these retailers to ‘rightsize’ but they remain critical to our UK high streets and also to the retail sector’s post-coronavirus recovery.

2 Readers' comments