The ring of the tills might be what drives retail, but to keep customers spending retailers need to invest in improvements. Retail Week looks at where some of the biggest – and most successful – retailers are directing their spend

While the cost-of-living crisis may be moderating, competition for share of spend is as ferocious as ever, with retailers committed to investing to maintain and enhance their appeal.

Tesco, for instance, will make a capital investment of £1.4bn this year. John Lewis, which is in the midst of a turnaround, is increasing its investment to £542m in 2024/25, up from £312m last year.

In the current climate, more than ever, any retail investment is necessarily accompanied by drives for efficiency and cost savings.

Pay

As inflation soared and unemployment remained low, pay rates turned into an arms race among big retailers as they sought to attract and retain the best staff.

While cost-of-living pressures are starting to ease, pay for frontline staff remains a battleground. Just last month, value grocer Lidl lifted its rate for hourly paid staff – for the third time in 12 months – to £12.40 an hour outside London and £13.65 in the capital, effective from June 1.

When it issued its full-year results in March, John Lewis Partnership said it would up overall pay this year by £116m – a “record investment”, according to the retailer.

It is a similar story elsewhere. From April this year, for instance, Tesco staff received a 9.1% rise in base pay – another “record investment” that amounted to approximately £300m.

Meanwhile, Marks & Spencer made its “biggest ever investment in frontline colleague pay” of £89m.

Retail Economics senior consultant Nicholas Found notes that the Bank of England expects pay growth to ease, but he expects it to remain at an elevated level throughout the year.

Tech and AI

When people cost more, retailers are unsurprisingly keen to make them as efficient and productive as possible, spending time on duties that make a difference to shoppers. Technology that helps achieve that is increasingly drawing investment.

In May, Sainsbury’s, for instance, unveiled a five-year partnership with tech giant Microsoft designed to “improve store operations, drive greater efficiency for colleagues and provide customers with more efficient and effective service, delivering stronger returns for shareholders”.

Sainsbury’s store staff will be able to use AI “to pull together multiple data inputs, such as shelf-edge cameras” to identify shelves in need of replenishment, therefore “saving valuable time as well as ensuring sales opportunities aren’t missed”.

The grocer’s initiative follows a similar one from M&S, which teamed up with SymphonyAI to use handheld devices to create “a connected-store environment, giving store colleagues prioritised tasks to quickly bring shelves into full planogram compliance”.

Tesco, meanwhile, is developing a “new range optimisation tool, which automates bespoke product selection based on store location and demographic”.

Tech investments are not restricted to AI. JLP is investing in technology “to improve customer service” and the customer experience of its eponymous department stores’ website in areas such as navigation.

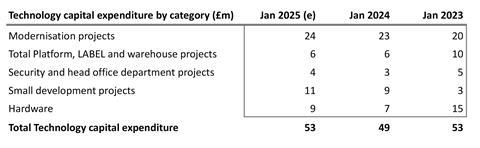

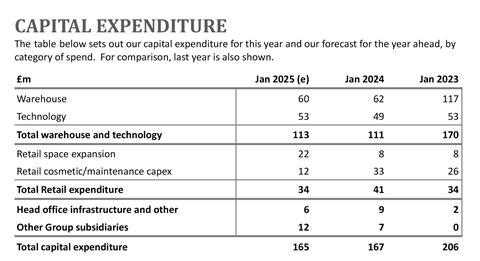

Next reported that its technology spend will peak at £216m this year, of which £53m will be capital spend.

The fashion giant intends to “steadily reduce this going forward” because “the aim is not just to save money; our intention is to spend less but deliver more new functionality”.

After £49m of capital spending on modernising and upgrading systems technology last year – £42m on software and £7m on hardware – Next expects that to rise in the current year to £53m.

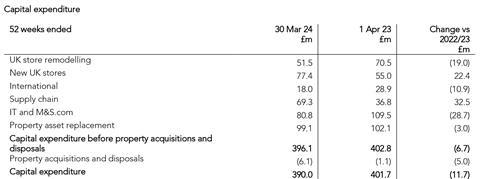

M&S spent £80.8m on technology and M&S.com last year, which includes everything from network upgrades to app development.

While much investment is going into established technology, Found still believes an increasing proportion will go to AI. He says: “It’s such early days, but it’s vital for retailers to think about it.”

Supply chain and automation

Key links in retailers’ supply chains such as warehouses are also being targeted for investment that improves efficiencies in the medium to longer term.

Tesco reported in its results that it has “started construction of a fresh food distribution centre in Aylesford, Kent, incorporating robotic automation technology”.

Sainsbury’s, which has just outlined the next phase of its ‘Save and invest to win’ cost programme, also sees opportunity in automation.

The grocer, which is targeting cost savings of £1bn by March 2027, said in its prelims in April: “High-returning investments in technology and automation will drive big steps forward in efficiency with more agile, flexible systems bringing greater efficiency to decision making and accelerating the speed at which we can bring improvements to customers.”

Next will spend about £60m this year on warehouse improvements, notably automation at its Elmsall 3 centre in Pontefract, where it is commissioning picking and packing automation that is expected to “deliver a step change in efficiency and capacity”.

M&S devoted £69.3m of capex to its supply chain last year, in areas such as expanding its clothing and home fulfilment.

Retail media

Tesco expects retail media to be “bigger than TV” by next year, according to a report in The Grocer on comments made at a recent IGD event.

The grocer is backing the growing media channel and aims to have 6,000 in-store digital advertising screens by the end of this year.

Tesco has also created a dedicated retail media team and tech stack as it leverages the power of its customer data to woo customers such as FMCG companies.

Sainsbury’s is building its own Nectar360 retail media operation and so far has approximately 800 screens.

Sainsbury’s said in its prelims: “We are investing in high-return growth by expanding our team and unifying our capabilities across in-store, onsite and offsite.”

These moves are part of a global trend. In February this year, Walmart showed how important it expects retail media to be when it announced it was spending $2.3bn (£1.8bn) to buy Vizio and its SmartCast operating system.

As well as providing Walmart with “new ways” to connect with customers such as in-home entertainment, the US retail giant says the deal brings “new opportunities to help advertisers connect with customers, empowering brands with differentiated and compelling opportunities to engage at scale and to realise greater impact from their advertising spend with Walmart”.

“Traditional retail margins are under pressure,” says Found. “Retailers need to engage in new services to bolster their margins.”

Stores and property

Bricks and mortar are still right at the heart of retailer investment.

Since 2019, for example, M&S has allocated £100m of capital to 12 new full-line branches as it targets “bigger, better stores” across its estate. This year, the retailer will open up to four.

Last year, M&S capex of £51.5m went to store remodelling and £77.4m on new shops.

Tesco opened net 87 stores last year – most of them in its core UK markets – and refreshed 389.

And John Lewis Partnership-owned Waitrose is beginning to open branches again for the first time in a decade.

Retailers’ spending continues to go in the direction of stores despite – and in some ways because of – the growing impact of technology.

As the pattern of online spending normalised following the pandemic, shops have taken on renewed importance and play a pivotal role in creating omnichannel appeal through services such as click-and-collect and returns.

In the words of M&S chief executive Stuart Machin, shops are a “competitive advantage for how customers want to shop today”.

Found says: “The composition of online sales has changed and the relevance of multichannel has become more significant. People want click-and-collect or to be able to return things to stores – it provides a layer of convenience.”

Prices and loyalty

Throughout the cost-of-living crisis, price has been at the centre of retail competition, especially in categories such as food, and investment in this area continues apace.

Just a couple of weeks ago, Morrisons cut and locked prices on another 400 items, from champagne to mushy peas.

Tesco cut prices on 4,000 products by an average of 12% last year. “Magnetic value for customers” is the grocer’s top strategic priority, so it is unlikely to take its foot off the pedal on price.

Tesco also exemplifies the determination of retailers to combine price with loyalty initiatives as it continues to build the appeal of Clubcard through member-only prices.

While investing in price and loyalty, Tesco aims to win a return on such investments by better leveraging the wealth of customer data it receives as a result, which also dovetails with initiatives such as building its retail media strength.

Sainsbury’s is taking a similar approach. Last year, it cut prices on commonly bought products by £220m and launched Nectar Prices. The adoption of Nectar is also helping to build its retail media business.

M&A

Tough times and hardships for many retailers have spelled opportunities for the strong.

Frasers Group, which owns Sports Direct as well as the eponymous department store and Flannels, has been well placed to snap up other businesses.

However, its purchases have not all gone well – Frasers paid £52m for Matchesfashion, but subsequently put it into administration, while a planned purchase of German retailer SportScheck was abandoned when it filed for insolvency.

Frasers has also bought stakes in retailers ranging from Currys to Boohoo, in the former case positioning itself as a kingmaker in the event of acquisition interest in the electricals giant.

Next has made a swathe of acquisitions as it builds its third-party Total Platform proposition. While there have been purchases of some distressed retailers, Next also snapped up Fat Face.

Privately owned retailer The Range, meanwhile, acquired the brand, website and intellectual property of bust variety store Wilko and is opening stores under that banner.

Alvarez & Marsal corporate transformation services managing director Erin Brookes believes 2024 may bring more deals – and not just for distressed assets.

Improving retail conditions and company valuations are among the factors that may stimulate activity.

In a column for Retail Week, she wrote: “These factors could create a sweet spot for deals in 2024, as cash-rich private equity funds and strategic investors look to pick up assets, particularly in sectors forecast to show strong growth.”

No comments yet